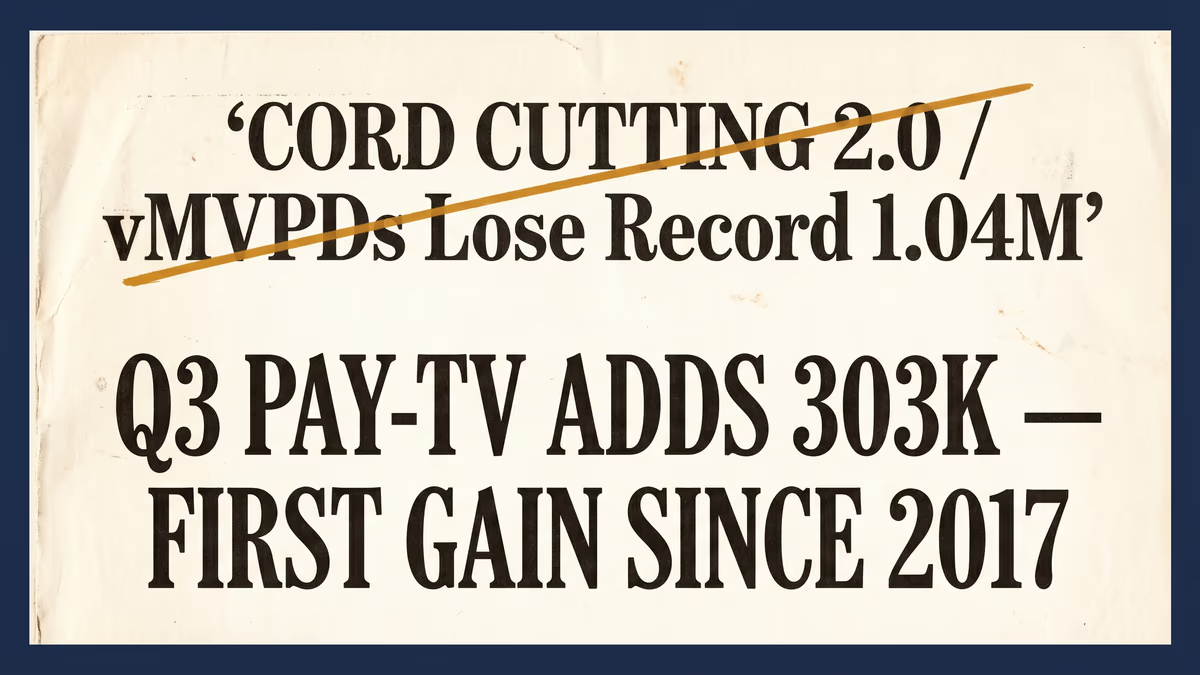

The most contradictory data point on the U.S. pay-TV table right now is one almost no trade desk is leading with: pay-TV added subscribers in the third quarter of 2025. Linear plus virtual, combined, MoffettNathanson’s Q3 Cord-Cutting Monitor counted a net gain of about 303,000, the first quarterly increase the analyst pair has logged since 2017. YouTube TV alone added 750,000. Aggregate vMVPD additions hit 1.43 million. The “Cord Cutting 2.0 inflection” framing every trade pub has been writing into 2026 is built around the opposite assumption.

The cable side of Q1 2026 just printed, and it does not bend the curve back. Comcast’s (NASDAQ: CMCSA) Q1 release showed the company shedding 322,000 video customers and 65,000 domestic broadband customers, both improvements over the year-ago quarter, when broadband alone bled 183,000. Charter (NASDAQ: CHTR) reported the next morning: residential video losses narrowed roughly two-thirds, from 181,000 a year ago to 60,000, even as broadband worsened to a 120,000 loss. Combined, the two largest U.S. MSOs lost 382,000 video subscribers in Q1 2026 against a comparable 668,000 last year. The cable-video cliff stalled.

That is a single-quarter read on two operators, not on its own the end of cord-cutting. But it is a real datapoint stacked on top of an even larger one (Q3 2025’s category-wide net add) and pointed in the opposite direction from a consensus narrative the industry has been recycling on a six-month lag. The MoffettNathanson Q1 2026 Cord-Cutting Monitor, which would supply the corresponding vMVPD aggregate, has not yet published. Until it does, the loudest “cord-cutting accelerates” headlines this week are working off a misread calendar: a 1.04 million vMVPD loss figure floating around trade coverage is from MoffettNathanson’s Q1 2025 Cord-Cutting Monitor reported by Light Reading last June, not anything the firm has published this quarter. Treating it as Q1 2026 data, as several pickup pieces have, is the kind of dating slip that produces a bigger consensus than the underlying evidence supports.

Why the cable line stopped falling as fast

Charter’s improvement has a name: the Hulu deal it expanded with Disney last June, which folded Hulu (with ads) into Spectrum TV Select at no upcharge and restored a pile of Disney-owned cable nets to the lineup after the 2023 dispute. The promise of that deal, that a cable subscriber’s bill could include Hulu without an itemized line, is exactly the proposition cord-cutters have been chasing for a decade. Charter is now four full quarters into running the experiment, and its quarterly video-loss number knifed two-thirds against the prior-year base. CEO Chris Winfrey has framed it consistently as a bundle-economics defense rather than a product reinvention, and the disclosure backs the framing: Charter doesn’t claim it’s adding video subs; it claims it’s keeping more of the ones it has.

Comcast’s improvement is harder to attribute to a single move. The Q1 video-loss line came in better than base, broadband losses narrowed materially against a Q1 2025 in which the end of the Affordable Connectivity Program had distorted the comp, and the company’s NewFronts pitch leans on “approach profitability” language at Peacock. None of those data points individually is a structural inflection. Together, they make it harder to argue that the cable side is rolling over faster, which is what “Cord Cutting 2.0” is supposed to imply.

Three quarters that don’t sit with the consensus narrative: Q3 2025 was a category gain. Q4 2025’s MoffettNathanson note never pulled into wide circulation. Q1 2026 has Comcast and Charter both improving, with the corresponding vMVPD print still pending. The cleanest read is that the consensus narrative is built off Q1 2025 trends — a real, brutal quarter — projected forward without intervening data.

The vMVPD side is the open question

Where the counter-consensus call gets harder is on the virtual-MVPD column. Q3 2025’s +1.43 million vMVPD add is real; it includes YouTube TV’s 750,000 quarter, the kind of print that suggests Google still controls the live-TV growth story when nothing else in the bundle is breaking. But two pieces of post-Q3 turbulence won’t show up cleanly until the next MoffettNathanson note: the Disney–YouTube TV blackout that pulled ESPN, ABC, FX, and the rest of the Disney cable suite for two weeks in late October and early November, and the Fubo–Disney close on Hulu + Live TV that produced a roughly 6.2 million-sub combined entity reporting under one cap. Either could distort a Q1 2026 vMVPD line in directions a “Cord Cutting 2.0” frame doesn’t anticipate: a churn spike at YouTube TV from the blackout, or a noisy first quarter of integrated reporting at the new Hulu + Live TV / Fubo entity.

EchoStar’s repricing response landed earlier this month. Sling Essentials launched at $19.99 a month with ESPN, ESPN2, Disney Channel, and nine other nets. It is the most explicit attempt by an incumbent vMVPD to reopen the price gap to cable that the category was originally built around. YouTube TV currently sits at $82.99; Hulu + Live TV at $88.99. The structural premise of the original 2015 vMVPD pitch, a skinny bundle priced to undercut the cable bill, has collapsed at the top of the market, and Sling is trying to rebuild it from the floor.

If the MoffettNathanson Q1 2026 vMVPD aggregate, when it publishes in the next couple of weeks, also comes in better than Q1 2025, even by a smaller margin than Q3, the “pause, not collapse” reading holds. If it comes in worse, the case is that Q3 2025 was a one-quarter blip driven by football season and the YouTube TV growth story, and the consensus framing reasserts. The publishing schedule, not the prose, will settle it.

The trade is the reframe

The market story most worth selling against the consensus is not that pay-TV is healthy. The combined Comcast-Charter video base still shrinks every quarter. Broadband at Charter is now bleeding faster than a year ago; Comcast’s wireless adds are doing real work covering the household relationship. The story is that the trajectory is improving on the cable side and was last seen adding on the combined side, which is structurally different from the “free fall” frame the headlines are running with. The consensus narrative is using Q1 2025 numbers and projecting them forward through a quarter that already broke the slope.

For ad buyers reading the streaming-wars retirement framing into upfront budgets, that distinction matters. The supply story is shifting toward ad-supported SVOD, but the linear-and-vMVPD base the upfront market still transacts against is not collapsing on the curve trade desks have penciled in. A combined pay-TV gain in Q3 2025, a stalled cable cliff in Q1 2026, and a still-pending Q1 vMVPD print is a different planning input than a doubled vMVPD loss the consensus has been pricing in for a quarter.

The data we have says the slope flattened. Watch the next MoffettNathanson note for whether the curve actually bent, or just paused.