Charter Communications (NASDAQ: CHTR) CFO Jessica Fischer raised the run-rate operating-synergy figure for the pending Cox Communications acquisition to $800 million on the April 24 earnings call, 60 percent above the $500 million Charter projected when the $34.5 billion deal was announced last year. Fischer attributed the raise to “procurement synergies, including programming, as well as better visibility into the financials.” That is the load-bearing data point from cable’s Q1 print, and most of the trade press buried it under merger chatter both companies spent their earnings calls swatting away.

The synergy lift came less than 24 hours after Comcast Corporation (NASDAQ: CMCSA) printed its first post-Versant Q1 and Co-CEOs Brian Roberts and Mike Cavanagh used the call to wave off cable M&A. Wall Street had spent the prior week packaging an analyst question on Charter’s call as merger-talks-resurfacing chatter. The actual data point the operators put on the tape says the strategy is broadband consolidation, not cable consolidation, and that the cord-cutting pause we wrote about last week is holding into Q2.

What the Cox-synergy raise actually says

Procurement synergies, the bucket Fischer named first, are operator code for programming-cost leverage. A bigger combined subscriber base buys down per-sub carriage rates with networks. That is the lever Charter used in 2023 to extract the transformative Disney deal that bundled Disney+ and ESPN+ into Spectrum Select while pulling eight smaller Disney cable channels off the lineup. It is the lever Charter is preparing to pull again, this time across a footprint that adds Cox’s roughly 5.5 million broadband subscribers to Charter’s existing base.

The math is the strategy. Combined Comcast plus Charter plus Cox would sit at roughly 63.7 million broadband subscribers, more than half of the U.S. fixed-broadband market by the household denominators trade research firms use. That is structurally tighter than the share the Department of Justice cited when it killed Comcast’s $45.2 billion bid for Time Warner Cable in 2015. The DOJ’s stated objection then was the broadband-gatekeeper concern. The same concern, on a bigger base, is the reason Comcast is choosing partnerships over a corporate combination today. Charter, with no geographic overlap and a willing private seller, can run the consolidation trade Comcast can’t.

The first post-Versant print

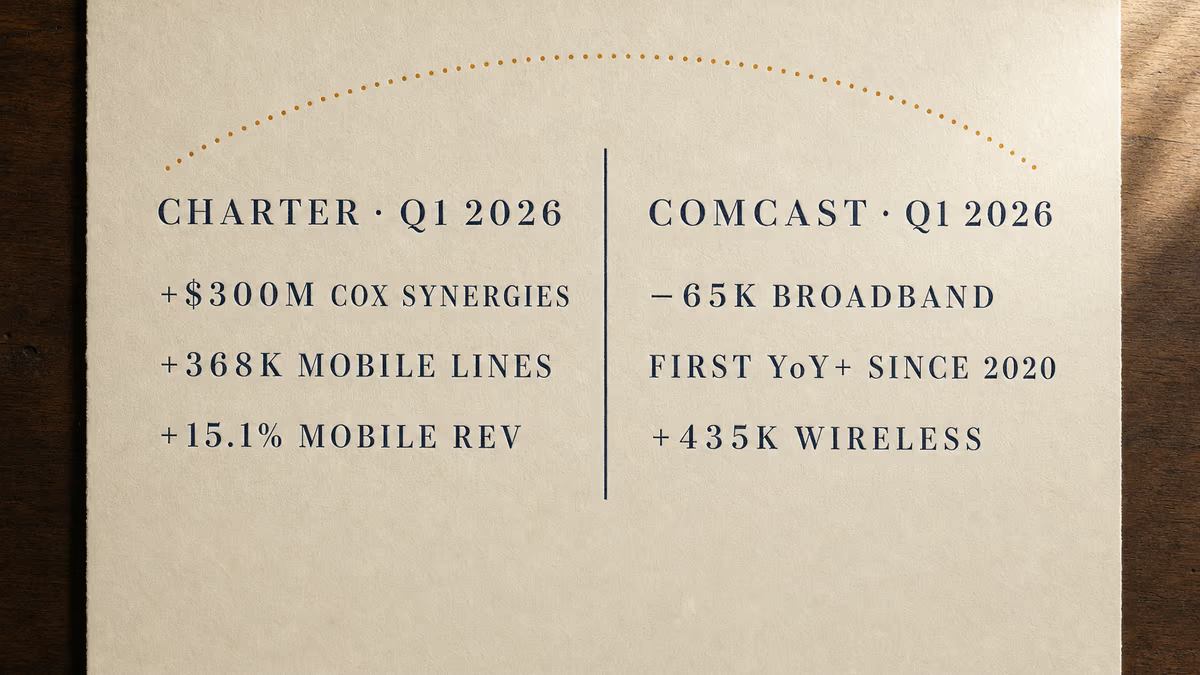

Comcast’s Q1 was the first quarterly disclosure since the Versant Media Group (NASDAQ: VSNT) spin completed in early January, which removed roughly $12.5 billion of assets and $4.3 billion of liabilities from the balance sheet and left Comcast with $94.6 billion of debt. Total revenue came in at $31.46 billion, up 5.3 percent year over year. Domestic broadband net losses landed at 65,000, narrow enough to qualify as the company’s first year-over-year improvement on broadband net adds since 2020 by management’s own framing. Wireless added a record 435,000 lines to reach 9.74 million on Xfinity Mobile.

Roberts and Cavanagh built the entire earnings-call narrative around reversing what Cavanagh called “the negativity around the cable segment.” On M&A, Cavanagh said the company is “open” to partnerships “around video or mobile,” and that Comcast has “plenty of opportunities to partner around video or mobile.” Roberts added: “The bar’s high, but we’re always focused on looking at those kind of creative situations. But that said, I also just really do like the direction of the company and don’t want to create a lot of distraction.”

The Versant spin is itself the strongest non-rhetorical signal here. If Comcast genuinely thought a Charter combination was near, separating $12.5 billion of cable networks first is unusual sequencing. Companies don’t typically pre-clean only their half of a hypothetical deal.

Spectrum Mobile is the re-anchor

The number that did the most work on Charter’s call was on the wireless side. Spectrum Mobile added 368,000 lines in the quarter to reach 12.1 million; mobile-service revenue grew 15.1 percent year over year to $1.05 billion. Combined with Comcast’s wireless print, the two operators added more than 800,000 mobile lines in three months on top of a roughly 21.8 million-line base, and they did it on MVNO rails (Verizon for residential, T-Mobile for the business-customer agreement signed last summer) rather than tower capex.

That is the convergence pitch with actual numbers behind it. It is also the bundle defense for the broadband-customer base. Charter narrowed video losses to 60,000 from 181,000 a year prior, a roughly 67 percent improvement that CEO Chris Winfrey attributed in part to the Hulu-bundle relaunch with Disney. But video revenue still fell 9.2 percent to $3.25 billion. The product is staunching subscribers and bleeding revenue at the same time.

For ad buyers, that is the line that prices the cable upfront. The customer is still there, mostly. The dollars per customer are not. Charter’s own ad revenue grew 5.3 percent in the quarter to $358 million, but that line is increasingly a political-ad and addressable story riding on the broadband-and-mobile customer relationship, not on the linear-cable subscriber. The pitch a buyer hears at the cable upfront and the pitch a buyer hears at NewFronts are converging on the same identity graph.

The chatter, and what the operators said about it

The merger framing traces to one analyst question on Charter’s call, amplified through a small group of trade outlets. No mainstream business press has reported either company is in talks. Winfrey’s own response named the structural fact that Charter has “no overlap” with Comcast, and Comcast’s Co-CEOs spent their own call saying they are not pursuing the deal. Deadline’s headline on the Comcast call read: “Comcast Not Exploring Cable Mergers.” Treat the chatter accordingly.

What buyers should price into the upfront

The May upfronts will be the first read on whether the cable-bundle inventory holds pricing against a video-revenue line down 9.2 percent. Charter is heads-down on closing Cox by summer, contingent on the California PUC clearing the last state hurdle ahead of the September 15 federal antitrust deadline. Comcast is heads-down on holding the broadband line into Q2 and proving Cavanagh’s “negativity” pitch wasn’t a one-quarter beat. Both companies just told you, in numbers, that the strategy for the next two years is bigger broadband footprints and bundled mobile. The Cox-synergy raise is the answer the operators keep giving to a question Wall Street keeps asking.