The structural disclosure thesis our preview previewed actually landed. Roku, Inc. (NASDAQ: ROKU) reported its first quarter under split Advertising and Subscriptions reporting after the bell Thursday, and the line that matters for advertisers is no longer buried inside a blended Platform number: $613 million in ad revenue, up 27 percent year-over-year, at a 60.5 percent gross margin. On the call, Roku Media President Charlie Collier put a flag on the strategy that disclosure now makes legible, telling analysts that ad spend through third-party programmatic platforms grew more than 40 percent year-over-year, with Amazon DSP, The Trade Desk, Yahoo, FreeWheel, and Google’s DV360 all named in the same breath. Roku raised its full-year Platform-revenue guide to roughly $5.0 billion. The stock added about 3.5 percent. The print itself was a beat; the structural read is the story. Roku is the only US public TV-OS company showing its ad math, and the math it is showing argues for the open stack.

First quarter results show our third-party DSP strategy is working. The majority of our video delivery is now through third-party programmatic partners, and we are growing quickly.

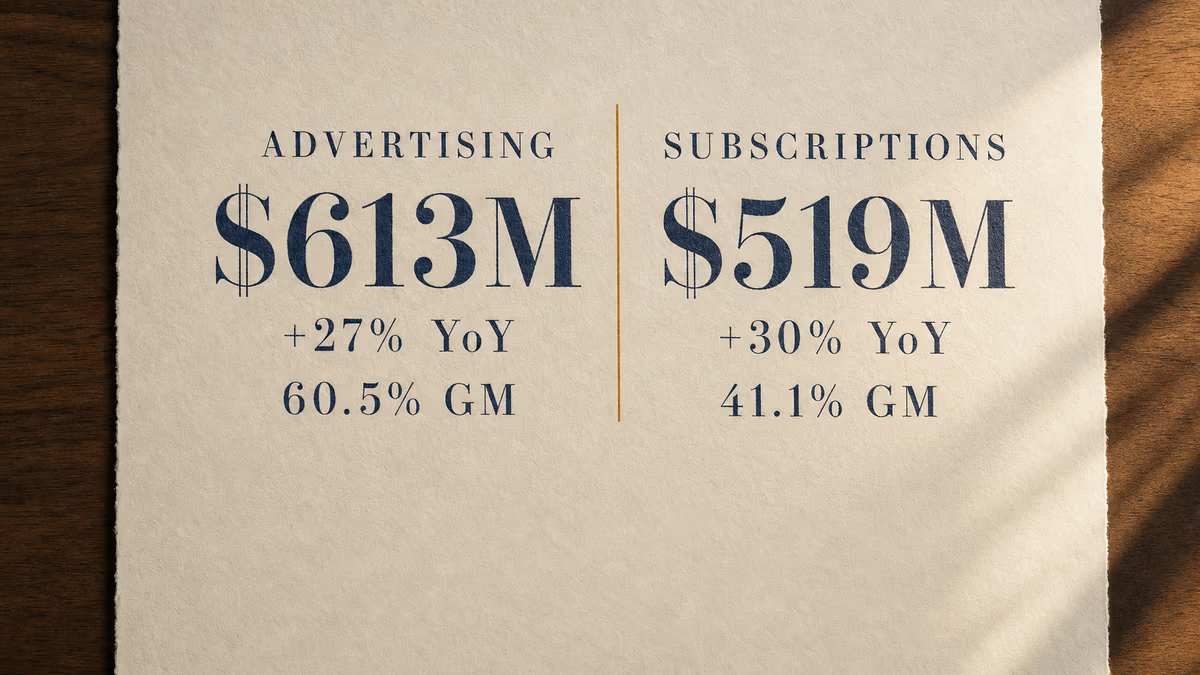

What the Advertising line tells you

Take the disclosure at face value for a beat. A $613 million ad business growing 27 percent at a 60.5 percent gross margin is more profitable per revenue dollar than Magnite, Inc. (NASDAQ: MGNI), more granular than The Trade Desk (NASDAQ: TTD), and more legible than the comparable line at any other US TV-OS company. CFO Dan Jedda told analysts that 60.5 percent margin level is sustainable for the rest of the year and thereafter. Subscriptions, the line nobody could see clearly under the blended Platform regime, came in at $519 million, up 30 percent (or roughly 23 percent excluding Frndly), at a 41.1 percent gross margin. Both lines are accelerating off restated FY 2025 bases the Cleveland Research analyst Ross Walthall pegged at +13 percent and +25 percent respectively, in a note reproduced by PPC Land before the print.

That comparison sharpens when you look around the room. Walmart Inc. (NYSE: WMT) consolidated VIZIO Holding Corp. into its Walmart U.S. segment in December 2024; the smart-TV ad business now reports as part of a global advertising line, with no segment dollar figure. Samsung Electronics has never disclosed Samsung Ads as a reportable segment. LG Ad Solutions sits inside LG Electronics’ Home Entertainment line. Amazon’s CTV mix is folded inside a $17 billion advertising services aggregate. Of the five biggest US TV-OS publishers, Roku is the one investors and buyers can underwrite at the segment level, and it just put up a higher gross margin than anyone they could compare it to.

Third-party DSP plumbing crosses a threshold

The more-than-40-percent line item is what turns a disclosure event into a strategy event. If the Advertising segment grew 27 percent and DSP-routed buys grew more than 40, third-party programmatic outpaced direct-sold inside the same quarter. Collier framed Roku’s positioning as “open, interoperable, and deeply integrated with every major DSP,” and named Amazon DSP, Trade Desk, Yahoo, FreeWheel, and DV360 as the five rails. The DV360 line carries some weight: Roku is the first streamer to participate in Google’s Confidential Publisher Match, which routes Google’s first-party signal through trusted-execution-environment matching directly into DV360-bought Roku inventory.

The Amazon DSP rail is its own complication, and worth flagging. Amazon spent the nine days before Roku’s print wiring its identity stack together: Acxiom Real ID audiences live in Audience Hub, Dynamic Traffic Engine donated to the IAB Tech Lab, Samsung Ads in Amazon Publisher Cloud. Amazon DSP being one of Roku’s named third-party buyers is the same Amazon hardening curation on its own protocol, with Roku’s open inventory as a buy-target. The two companies are competing for the same demand and routing the same demand through each other. That is what plumbing looks like when nobody owns the whole pipe.

Why Roku Curate is the operational footprint

Three days before the print, Roku launched Roku Curate, a curated marketplace bundling Roku first-party data with retail-purchase signal from six launch partners (Best Buy Ads, Criteo, Fandango, Fetch, Instacart, and Kroger Precision Marketing), powered in part by Magnite’s SpringServe ad server and Roku’s own exchange infrastructure. The timing was not casual. Curate is the product that proves the segment-split is a posture, not a GAAP rearrangement. It uses the SSP layer (Magnite SpringServe) without ceding the buyer relationship; it assembles the not-Walmart retail-data graph in one direct-sold package; and it ships during the same week Roku’s first segment-itemized P&L hits the wires.

Read it against the walled-garden map and the bet sharpens. Walmart Connect plus VIZIO offers retail-data inside a closed Walmart pipe. Amazon DSP plus Acxiom plus Samsung Ads-in-APC offers identity inside a closed Amazon graph. Roku Curate plus six retail-data partners plus five named DSP rails offers the same composite signal without the closed pipe. Roku is selling the open option to ad buyers who do not want to underwrite a single hyperscaler, and it is doing it on margin economics that, on the Advertising line, beat the SSPs that supply it.

Three Q1 prints sit in Roku’s gravity now

The next seven days frame the gravity. Magnite reports Q1 results after the bell next Wednesday, May 6, and is the most directly exposed publisher-side read: Magnite SpringServe + Magnite Streaming SSP underpin Roku Exchange, power Roku Curate, and benchmark against Magnite’s Q1 guide of CTV contribution-ex-TAC at $81 to $83 million. Trade Desk and PubMatic, Inc. (NASDAQ: PUBM) both report after the bell Thursday, May 7. TTD now has a Roku-disclosed denominator to size its CTV exposure against, and the Ventura Ecosystem framing gets to be tested against a publisher openly routing more than 40 percent more of its inventory through DSPs including TTD. PubMatic, with omnichannel video at 39 percent of FY 2025 revenue, has the open-stack tailwind that Roku just monetized in public. Then the May 11–14 upfront cycle — NBCUniversal and Amazon on May 11, Disney on May 12, YouTube Brandcast on May 13, Netflix on May 14 — gives Amazon, Samsung, and LG their first major stages to respond to Roku having put public dollar signs on a category none of them disclose.

The financial profile underneath is real and helps. EPS came in at $0.57 against a $0.35 Street estimate; trailing-twelve-month free cash flow hit an all-time high of $538.8 million; adjusted EBITDA was $148.4 million, up 165 percent. Wall Street rolled into the print and lifted price targets (Wedbush to $155, Morgan Stanley to $135, Benchmark to $160) the morning after. None of that is the lede. The lede is that for the first quarter Roku has been a public company, an ad buyer can read its ad business as an ad business, and the read is structurally at odds with how every other US TV-OS company has chosen to report.