The format is recognizable from across the room. Open the redesigned Netflix iPhone app, tap the new Clips tab in the bottom navigation, and you drop into a vertical, swipeable feed of short cuts from the Netflix catalog: a TikTok-shaped hole inside a long-form streaming product. The launch went live in nine markets on April 30 with a press release from Chief Product and Technology Officer Elizabeth Stone framing the format as “a personalized highlight reel that helps you decide what to watch or play next, without endless scrolling.” Stone, speaking to TechCrunch, was careful: Netflix “is not intending to copy or chase exactly what a TikTok or others are doing.”

The disclaimer is honest about format and quiet about pattern. Clips is a discovery primitive, not a content format — Variety’s launch-day subhead is the load-bearing detail: full-length Netflix shows and films still require landscape orientation. What Netflix imported isn’t TikTok’s vertical-video catalog. It’s TikTok’s navigation gesture, the algorithmically-ranked thumb scroll, with a Watchlist save and a share button bolted on. And every other app that imported that gesture monetized it within 24 months.

The concession Greg Peters made before the launch

The clearest read on why Clips ships now didn’t come from the Stone press release. It came two weeks earlier on Netflix’s Q1 2026 earnings call, when Co-CEO Greg Peters explained the company’s parallel push into video podcasts. “Podcast consumption indexes to daytime hours on Netflix,” Peters said, “which allows us to capture a time when we historically have less engagement. The other is that it indexes much more to mobile.” Co-CEO Ted Sarandos, on the same call, called mobile a place where “professional TV and film historically make up a small percentage” of viewing.

Read those two sentences together and the strategic posture is named explicitly: Netflix has a daytime mobile gap. The Tudum app’s hours are the evening-couch hours, not the lunch-break hours. Podcasts and Clips are two answers to the same problem.

Antenna’s reading of the broader market sharpens why now. Premium SVOD subscriber growth fell to 7% in 2025, the first single-digit year on record. With sub growth capped, the competitive surface reframes around two axes: ARPU expansion through ad tiers, and per-user engagement through time-on-app. Netflix’s Amazon and Yahoo programmatic-targeting layers go live for the May 14 upfront. That’s the ARPU axis. Clips is the engagement axis. They land within a fortnight of each other for a reason.

The pattern incumbent apps keep repeating: Snap shipped Discover in January 2015. YouTube launched Shorts in beta in September 2020. Instagram launched Reels the same month. Spotify rolled vertical discovery to 500 million users as the default home view in early 2023. ESPN added a vertical feed last August. Disney+ shipped Verts on March 12 — 49 days before Clips. The motion across an 11-year arc and roughly nine platforms is identical: an incumbent app with established time-spent embeds the discovery gesture of a faster-growing competitor to capture the gap-time minutes the incumbent isn’t serving.

What Fast Laughs taught Netflix the hard way

Netflix isn’t new to this trend. It’s new to taking it seriously. The first attempt, Fast Laughs, shipped in March 2021: comedy-only, mobile-only, hidden in a side menu. It made it to TVs in early 2022 and was quietly discontinued sometime last year after low engagement. A 2024 follow-up, Netflix Moments, repositioned the format as a social-share tool rather than a discovery surface. Both were hedges, and both told the same story: the discovery gesture is hard to retrofit when the underlying catalog isn’t catalog-of-creators-making-vertical-content.

Clips is the inverse posture. Bottom-nav real estate next to Search. The full Netflix catalog as the source pool. A press release in the CPTO’s name. A Co-CEO admission on the earnings call that the format addresses an engagement problem the company concedes exists. The hedging is gone.

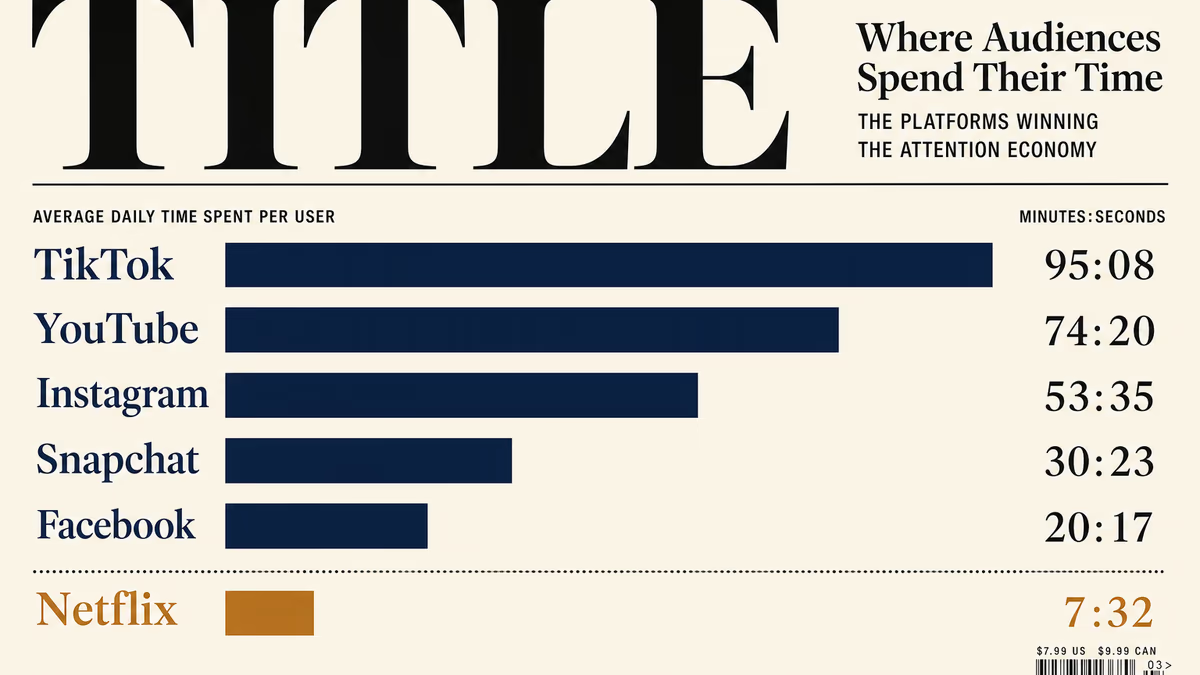

The size of the prize that Clips chases is real, but it’s also peaking. eMarketer projects TikTok’s average daily minutes per US adult user at 52 in 2025, down 6.9% year-over-year, the format’s first documented contraction. YouTube Shorts is still climbing fast: 200 billion daily views in Q1, up from 70 billion two years ago. The total short-form pie is still expanding, but TikTok’s per-user share is no longer growing on its own. The capacity for a credible new vertical surface to take share has rarely been more open.

The discovery-economics question Netflix won’t answer in public

Netflix’s published framing is that Clips is a recommendation tool. Stone’s release: helping you “decide what to watch or play next.” Peters’ earnings remarks on the broader recommendation push: “newer model architectures” let the company “iterate and improve more quickly.” Both true. Both insufficient as the whole story.

A vertical, algorithmically-ranked, swipe-able feed is also the most monetizable canvas in mobile advertising. Three things make it so:

- Native ad unit. A 9:16 ad slot rendered between organic clips is indistinguishable in form from the surrounding content. TikTok’s, Reels’, and Shorts’ core formats are all this exact unit.

- Personalization signal density. Every swipe is a vote. Watch-time, repeat-views, and skips at the per-clip granularity feed a recommendation model that doubles as an ad-targeting model.

- Frequency at the gap-time slot. The minutes Netflix is trying to claim (commute, lunch, in-line-at-the-store) are the highest-frequency, lowest-friction ad windows available.

Netflix now operates an ad business with more than 4,000 advertisers, 60%+ of new sign-ups in ad markets choosing the ad tier, and ad revenue tracking to roughly $3 billion in 2026. The targeting integrations with Amazon DSP, Yahoo DSP, and The Trade Desk are live or going live. The infrastructure to monetize a vertical-feed surface is sitting next to Clips. The DoubleVerify TikTok measurement-currency standardization we covered in April means the buy-side data plumbing for short-form already exists.

There are no ads in Clips at launch. There is also no public Netflix commitment that there won’t be.

What to watch next

The cleanest tell will be Q2 itself. The May 14 upfront opens with Netflix’s targeting depth at its newest peak; if the company introduces Clips as inventory in the same window, the discovery framing will be retrofitted around an ad story. If the surface stays ad-free through the summer, Netflix is buying optionality on monetization while it tests the engagement bar. Disney+ is the comparison: Verts has been live seven weeks and Disney has disclosed nothing beyond “additional engagement.” A real number from either company is the next analytical hinge.

The other hinge is geography. Clips is iPhone-only and lives in nine markets, two of which (India, the Philippines) are Android-first. The format only matters at the size Netflix needs it to matter if the Android rollout lands fast.

The strategic line from Peters is the one to file: mobile is where Netflix has historically had less engagement. Clips is the company’s argument that the answer is to copy the gesture that won every other app’s mobile-time-spent battle, and trust that the second-order question (what happens to the format when an SVOD owns it) sorts itself out later.