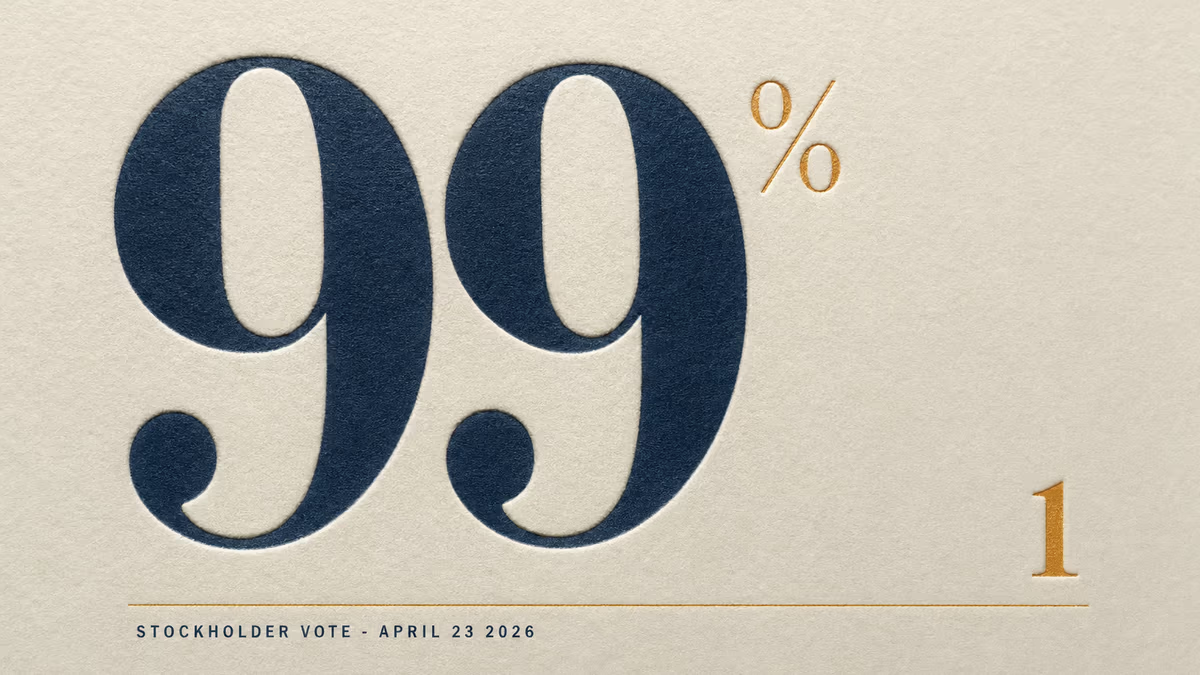

Warner Bros. Discovery (NASDAQ: WBD) shareholders adopted the company’s merger agreement with Paramount Skydance Corporation (NASDAQ: PSKY) on April 23 by a margin of 1,742,843,087 to 16,260,135 — roughly 99 percent of votes cast and 70.3 percent of outstanding shares present, WBD disclosed in an 8-K filing the same day. The vote clears the principal corporate hurdle on a $31-per-share, all-cash transaction WBD’s board had endorsed in February. The company is targeting a Q3 2026 close, it said in a press release, subject to remaining regulatory clearances.

For ad buyers, the calendar is what matters. The IAB NewFronts begin in 12 days. The 2026 upfront cycle is the last in which WBD and Paramount sell separately, as The Hollywood Reporter has noted, because the merger does not close in time to merge their pitches this season. By next May, holding-company buyers will be negotiating against a streaming front line of four sellers, not five: Netflix (NASDAQ: NFLX), Disney, the combined HBO Max plus Paramount+ entity, and a Comcast-and-Amazon tier.

The shareholders also rejected, on a nonbinding advisory vote, the merger-related compensation packages for David Zaslav and other named executive officers. Of votes cast, 1,444,387,748 shares opposed the package and 307,742,302 supported it, per the same 8-K, or roughly 82 percent against. Variety, citing the WBD definitive proxy, pegged Zaslav’s package at $34.2 million in cash severance plus $517.2 million in equity in the combined company and up to $335 million in potential tax reimbursement, with JB Perrette, Bruce Campbell, Gunnar Wiedenfels, and Adam Zeiler also receiving nine-figure exits. The advisory rejection does not bind the board.

The two-suitor chapter closes in a single quarter

The April 23 vote ratifies the second of two competing acquisitions of WBD that ran inside Q1 2026, resolving both arcs in the same window.

WBD signed a cash-and-stock merger with Netflix on December 5, 2025, then declared Paramount’s $31 hostile bid superior on February 26, terminated the Netflix agreement on February 27, and signed with Paramount Skydance the same day. Paramount Skydance, on behalf of WBD, paid Netflix the $2.8 billion termination fee owed under the broken agreement, Netflix disclosed in Note 6 of its Q1 2026 10-Q. The fee landed in Netflix’s “Interest and other income (expense)” line and helped lift Q1 net income to $5.28 billion, an 83 percent year-over-year increase, per Variety. On April 22, the day before the WBD vote, Netflix’s board authorized an additional $25 billion share repurchase. Co-CEOs Ted Sarandos and Greg Peters said in a Netflix statement after the deal collapsed that the WBD transaction “was always a ‘nice to have’ at the right price, not a ‘must have’ at any price,” as Variety reported at the time.

Two companies that wanted WBD ended Q1 2026 in opposite postures — Paramount Skydance bound to a closing it must defend through global regulators, Netflix returning capital to shareholders. Both stories run through the same balance-sheet item.

Four sellers, not five, at NewFronts

The combined-company asset map is the only one that matters at NewFronts. Two streaming services with roughly 50 million overlapping U.S. subscribers, per eMarketer; two news organizations (CNN and CBS News); two sports portfolios (TNT Sports’ NBA international, MLB, and NHL packages alongside CBS Sports’ NFL AFC and March Madness rights); and two FAST-and-cable inventory pools, including Pluto TV. The cable bundle alone — HGTV, Food Network, Discovery, TNT, TBS, truTV, Nickelodeon, MTV, Comedy Central, BET — is the largest single-owner ad-supported linear footprint in the U.S. market.

eMarketer principal analyst Marisa Jones, writing days before the vote, told eMarketer: “Marketers do have, at the very least, more ad support environments and leverage as ad buyers with this deal.” Her colleague Ross Benes, in the same eMarketer piece, called the consolidation “more attractive for marketers” and predicted Discovery+ would not survive as a standalone product two years out. The buyer-side argument cuts both ways. A combined HBO Max plus Paramount+ ad-sales pitch widens the inventory pool a single buy can address. That is useful when budgets are unified and less useful when category exclusivity is the constraint. Concentration always favors the seller at the next negotiation; it favors the buyer only at the current one, when the combined entity is still motivated to lock in commitments.

That tension is why the 12-day window before NewFronts is the actual story. Paramount Skydance opened upfront client dinners on April 16 under newly installed CRO Jay Askinasi, Adweek reported. His pitch, by Adweek’s account, leans on a “streaming fixed unit” sponsorship product and opens sports inventory to programmatic insertion. That is the pitch of a merged seller, even though Paramount cannot legally merge the inventory yet. How Paramount Skydance stages the NewFronts pitch will be the first signal of the merged ad-sales organization, particularly whether it presents alongside WBD or runs in parallel. JB Perrette, WBD’s CEO of Global Streaming and Games, told Screen Daily and Broadcast in February that “more is not better; better is better.” That posture, articulated by the executive who built HBO Max into a global premium streaming pitch, is precisely the asset David Ellison is now buying. Whether it survives integration with Paramount+, which is closer to the catalog-scale model, is the open question.

The gates that remain are not the FCC

The shareholder vote settles the deal-economics question and removes one closing condition. The remaining gates are regulatory and structural. The U.K. Competition and Markets Authority pre-notification comment period closes April 27. The European Commission has not yet announced a formal review. California Attorney General Rob Bonta has an open investigation; multiple state AGs are reported to be weighing action under a Nexstar–Tegna-style theory, Variety reported. The Federal Communications Commission is the gate that is not a gate: WBD owns no broadcast licenses, and FCC Chair Brendan Carr has signaled publicly that the agency expects to play no meaningful role in the transaction. The slate of approvals that delayed the Skydance–Paramount close last summer, including the CBS News ombudsman commitment and the DEI condition, does not have an analogue here.

The compensation rejection is the louder governance signal. WBD’s board can pay Zaslav anyway; the vote is advisory. But an 82 percent rejection on a Big-4 media company’s exit pay package, on the same day shareholders approved the deal that triggers it, is the kind of split decision that proxy advisors will cite for years. Erik Gordon of the University of Michigan Ross School, on Variety’s Daily Variety podcast, said the transaction “will probably come to symbolize all of those big changes.” The vote tally underneath that framing reads cleanly: shareholders endorsed the strategic logic and refused to underwrite its architects.

The Q3 2026 close target gives buyers and sellers two more upfront-adjacent quarters of clarity. NewFronts on May 5 is the first read. The four-seller streaming market starts setting prices in earnest at the combined company’s first post-close earnings call and at the first integrated upfront pitch in spring 2027.